What is "Lack of recent installment loan information" 101

In today’s dynamic financial landscape, the availability of accurate and up-to-date information is crucial for consumers seeking lack of recent installment loan information. Unfortunately, there is a noticeable gap in recent information about these financial products.

Understanding the Lack of Recent Installment Loan Information

In today’s dynamic financial landscape, the availability of accurate and up-to-date information is crucial for consumers seeking installment loans. Unfortunately, there is a noticeable gap in recent information about these financial products. This article aims to provide comprehensive details on installment loans, their benefits, and the current state of information, addressing the lack of recent data and helping consumers make informed decisions.

What Are Lack of recent installment loan information?

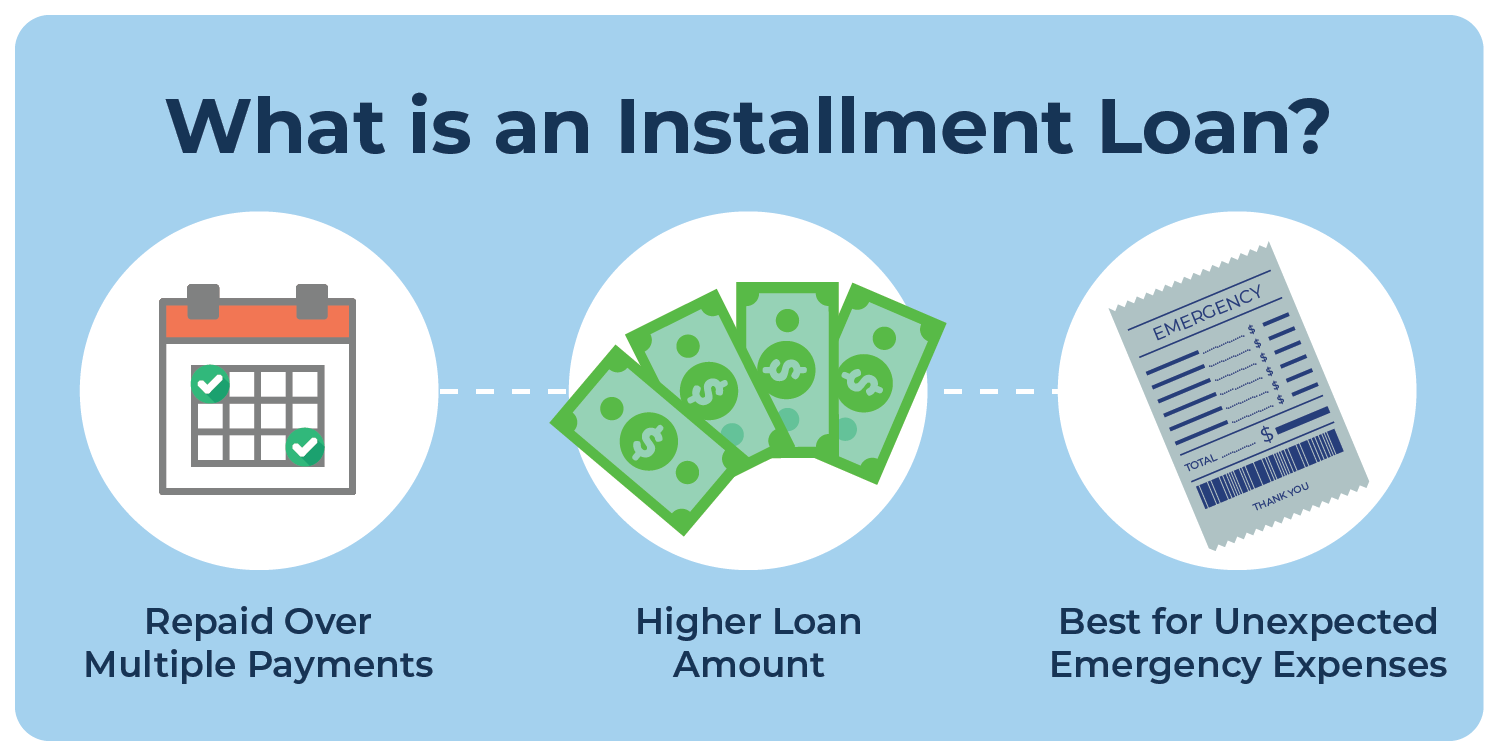

Installment loans are a type of loan where the borrower receives a lump sum of money upfront and agrees to repay the loan in fixed, regular payments over a specified period. These loans are often used for significant expenses such as home improvements, medical bills, or debt consolidation. They differ from revolving credit, such as Lack of recent installment loan information credit cards, in that the repayment terms and amounts are predetermined.

Types of Installment Loans

There are several types of installment loans, each catering to different financial needs:

- Personal Loans: Unsecured loans that can be used for various purposes, from debt consolidation to unexpected expenses.

- Auto Loans: Secured loans specifically for purchasing a vehicle.

- Mortgages: Long-term loans used to purchase real estate, with the property serving as collateral.

- Student Loans: Loans designed to cover educational expenses, often with more favorable terms for students.

Personal Loans

Personal loans are highly versatile and can be used for a myriad of purposes. Because they are typically unsecured, meaning they do not require collateral, the interest rates tend to be higher compared to secured loans. Personal loans are popular for consolidating high-interest debt, covering unexpected medical expenses, or financing significant life events like weddings or vacations.

Interest Rates and Terms: Personal loan interest rates vary widely depending on the borrower’s creditworthiness, ranging from as low as 5% to as high as 36%. Repayment periods typically range from 12 months to 84 months. Borrowers with higher credit scores generally receive more favorable terms.

Eligibility Criteria: Lenders assess several factors when determining eligibility for personal loans, including credit score, income, employment status, and debt-to-income ratio. Many lenders require a minimum credit score of 600, but this can vary.

Auto Loans for Lack of recent installment loan information

Auto loans are secured loans specifically intended for purchasing vehicles. The vehicle itself serves as collateral, which can result in lower interest rates compared to unsecured personal loans.

Interest Rates and Terms: Interest rates on auto loans can range from 3% to 10% or more, depending on the borrower’s credit score and the loan term. Loan terms typically range from 36 to 72 months, with some lenders offering terms up to 84 months.

New vs. Used Cars: Interest rates can differ for new and used cars, with new car loans generally offering lower rates. However, new cars depreciate faster, so it’s important to consider the overall cost of the loan and the vehicle’s depreciation.

Mortgages

Mortgages are long-term loans used to purchase real estate. These loans are secured by the property being purchased and typically come with much longer repayment terms, ranging from 15 to 30 years.

Types of Mortgages: There are various types of mortgage loans, including fixed-rate mortgages, adjustable-rate mortgages (ARMs), Federal Housing Administration (FHA) loans, and Veterans Affairs (VA) loans. Each type has distinct features and eligibility criteria.

Interest Rates and Terms: Fixed-rate mortgages offer a consistent interest rate throughout the loan term, providing stability in monthly payments. Lack of recent installment loan information, ARMs typically start with lower interest rates that adjust periodically based on market conditions, which can be beneficial if rates decrease but risky if they increase.

Down Payments: The size of the down payment can significantly affect the mortgage terms. Larger down payments often result in lower interest rates and eliminate the need for private mortgage insurance (PMI).

Student Loans

Student loans are designed to help cover educational expenses, including tuition, books, and living expenses. They come in two main types: federal student loans and private student loans.

Federal Student Loans: These loans are funded by the federal government and typically offer more favorable terms than private loans, including lower interest rates and flexible repayment options. Types of federal loans include Direct Subsidized Loans, Direct Unsubsidized Loans, and PLUS Loans.

Private Student Loans: Offered by private lenders, these loans often require a credit check and may have higher interest rates than federal loans. Lack of recent installment loan information, They can be a good option for covering expenses not met by federal loans.

Repayment Plans: Federal student loans offer various repayment plans, including income-driven repayment plans that adjust monthly payments based on the borrower’s income and family size. Private loans typically have less flexible repayment options.

Benefits of Installment Loans

Predictable Payments

One of the primary advantages of installment loans is the predictability of payments. Borrowers know exactly how much they need to pay each month, which helps in budgeting and financial planning. This stability can provide peace of mind and allow for better financial management.

Fixed Interest Rates

Most installment loans come with fixed interest rates, meaning the rate does not change over the life of the loan. Lack of recent installment loan information, This stability can be particularly beneficial in an economic climate with fluctuating interest rates. Fixed rates allow borrowers to lock in a favorable rate, avoiding the risk of increasing interest costs.

Credit Building by Lack of recent installment loan information

Timely repayment of installment loans can positively impact your credit score. Since the repayment schedule is fixed, it is easier to manage payments, contributing to a healthier credit profile. This can be especially beneficial for those looking to build or rebuild their credit.

Large Loan Amounts for Lack of recent installment loan information

Installment loans can provide access to significant sums of money, making them ideal for large expenses like home renovations, medical bills, or purchasing a car. Lack of recent installment loan information, This can be more convenient than using multiple smaller loans or revolving credit options.

Lower Interest Rates Compared to Credit Cards

Installment loans often offer lower interest rates compared to credit cards, especially for borrowers with good credit. This can make them a more cost-effective option for financing larger purchases or consolidating high-interest debt.

The Current State of Installment Loan Information

Despite the importance of installment loans, there is a significant lack of recent information available to consumers. This gap can be attributed to several factors, including rapid changes in the financial industry, Lack of recent installment loan information the emergence of new loan products, and evolving regulations.

Impact of Rapid Financial Changes

The financial sector is continually evolving, with new products and services being introduced regularly. This rapid pace of change can make it challenging for information to stay current, leaving consumers with outdated data that may not reflect the latest loan options or terms. For example, the rise of fintech companies has introduced new lending platforms that offer innovative products not covered by traditional financial information sources.

Emergence of New Loan Products

Innovative loan products are continually being developed to meet diverse consumer needs. For example, the rise of fintech companies has introduced new lending models, such as peer-to-peer loans and digital-only banks offering installment loans with unique features. This innovation can outpace the availability of updated information. Additionally, Lack of recent installment loan information, new credit scoring models and underwriting criteria are being implemented, which can affect loan approval and terms.

Regulatory Changes at Lack of recent installment loan information

Regulatory changes can significantly impact the availability and terms of installment loans. Governments and financial authorities frequently update regulations to protect consumers, which can result in modifications to loan offerings. Keeping up with these changes requires constant monitoring and updating of information. Lack of recent installment loan information, For instance, changes in interest rate caps, lending practices, and consumer protection laws can all influence the terms and availability of installment loans.

Economic Conditions for Lack of recent installment loan information

Economic conditions play a crucial role in the lending landscape. Factors such as interest rate fluctuations, inflation, and employment rates can influence both the demand for and the availability of installment loans. During economic downturns, lenders may tighten their lending criteria, making it more difficult for consumers to obtain loans. Conversely, in a strong economy, there may be more favorable loan terms available.

Bridging the Information Gap

To address the lack of recent installment loan information, several steps can be taken:

Regular Updates from Financial Institutions

Financial institutions must prioritize updating their loan information regularly. This includes interest rates, repayment terms, and eligibility criteria. Providing consumers with the latest data can help them make informed decisions. Banks and lenders should also improve their communication channels, ensuring that customers have easy access to current information through websites, mobile apps, and customer service representatives.

Enhanced Financial Literacy Programs

Increasing financial literacy among consumers is essential. Financial institutions, non-profits, and government agencies should collaborate to offer educational programs that explain the intricacies of installment loans and how to choose the right loan product. Workshops, online courses, and informational brochures can help consumers understand their options and the factors that influence loan terms and eligibility.

Leveraging Technology

Utilizing technology can streamline the dissemination of information. Financial institutions can employ AI and machine learning to provide personalized loan recommendations based on the latest data. Additionally, mobile apps and websites should be regularly updated with new information. Chatbots and virtual assistants can offer real-time assistance, answering common questions and guiding users through the loan application process.

Transparent Communication

Transparency is key in financial services. Financial institutions should ensure that all terms and conditions are clearly communicated to potential borrowers. This includes any changes to loan products or new offerings. Providing clear, concise, and easy-to-understand information can help consumers make more informed decisions and avoid potential pitfalls.

Partnerships with Financial Educators

Collaborating with financial educators and advisors can enhance the quality and reach of installment loan information. These professionals can offer personalized advice, helping consumers navigate the complexities of the lending landscape. Financial institutions can partner with schools, community organizations, and online platforms to provide educational resources and guidance.

Improved Regulatory Oversight

Governments and regulatory bodies should ensure that financial institutions comply with transparency and consumer protection standards. Regular audits and reviews can help maintain the integrity of the information provided to consumers. Regulations should also encourage the timely updating of loan information to reflect current market conditions and legal requirements.

Consumer Advocacy Groups

Consumer advocacy groups play a vital role in bridging the information gap. These organizations can provide independent, unbiased information and resources to help consumers make informed decisions. Advocacy groups can also lobby for better transparency and fair lending practices, ensuring that consumers have access to accurate and up-to-date information.

Choosing the Right Installment Loan

When considering an installment loan, it is essential to evaluate several factors to ensure you select the best option for your needs:

Interest Rates

Compare interest rates from different lenders to find the most competitive option. Even a small difference in rates can significantly impact the overall cost of the loan. Look for lenders that offer prequalification, allowing you to see potential rates without impacting your credit score. Consider both fixed and variable rate options, depending on your financial situation and risk tolerance.

Repayment Terms

Consider the length of the repayment period and the amount of the monthly payments. Choose a term that fits comfortably within your budget. Longer terms may result in lower monthly payments but higher overall interest costs. Shorter terms typically have higher monthly payments but lower total interest paid over the life of the loan.

Fees and Penalties

Be aware of any fees associated with the loan, such as origination fees or prepayment penalties. These can add to the cost of the loan and should be factored into your decision. Other potential fees to consider include late payment fees, processing fees, and annual fees. Understanding all the costs involved can help you make a more informed decision.

Lender Reputation

Research the reputation of the lender. Look for reviews and ratings from other borrowers to ensure you are working with a reputable institution. Check for any complaints or legal actions against the lender. A lender with a strong reputation is more likely to offer fair terms and excellent customer service.

Loan Purpose

Clearly define the purpose of the loan and ensure that the loan terms align with your financial goals. For example, if you are consolidating debt, ensure that the new loan offers a lower interest rate and better terms than your existing debt. If you are financing a large purchase, consider how the loan fits into your overall financial plan.

Credit Score Impact

Understand how the loan will impact your credit score. Applying for a new loan can result in a hard inquiry, which may temporarily lower your credit score. However, timely payments can help improve your credit over time. Consider the short-term and long-term effects on your credit profile when choosing a loan.

Additional Benefits

Some lenders offer additional benefits or features that can enhance the value of the loan. For example, some personal loans come with flexible payment options, hardship programs, or interest rate discounts for autopay. Evaluate these features to determine if they provide added value.

The Role of Fintech in the Installment Loan Market

The rise of fintech has significantly transformed the installment loan market. Fintech companies leverage technology to offer innovative lending solutions that cater to a wide range of consumers. These companies often provide faster approval processes, more flexible loan terms, and enhanced customer experiences.

Peer-to-Peer Lending

Peer-to-peer (P2P) lending platforms connect borrowers directly with individual investors. This model can result in more competitive interest rates and a streamlined application process. P2P lending has grown in popularity due to its potential for lower rates and more personalized lending experiences.

Digital-Only Banks

Digital-only banks, also known as neobanks, offer installment loans through entirely online platforms. These banks often have lower overhead costs, allowing them to offer competitive rates and terms. The convenience of managing loans through mobile apps and websites appeals to tech-savvy consumers.

AI and Machine Learning

Fintech companies use AI and machine learning to enhance the lending process. These technologies can improve credit risk assessment, provide personalized loan recommendations, and streamline the application process. AI-driven chatbots and virtual assistants can offer real-time support, answering questions and guiding borrowers through the loan process.

Blockchain Technology

Blockchain technology has the potential to revolutionize the installment loan market by providing secure, transparent, and tamper-proof records of transactions. This can enhance trust between borrowers and lenders, reduce fraud, and streamline the loan approval and repayment process.

Alternative Credit Scoring Models

Traditional credit scoring models may not accurately reflect the creditworthiness of all consumers. Fintech companies are developing alternative credit scoring models that consider a broader range of data points, such as social media activity, payment history on utilities and rent, and other non-traditional metrics. Lack of recent installment loan information, These models can help expand access to credit for underserved populations.

Regulatory Considerations for Installment Loans

Regulatory oversight is essential to ensure fair lending practices and protect consumers. Several key regulations impact the installment loan market:

Truth in Lending Act (TILA)

The Truth in Lending Act requires lenders to provide clear and concise information about the terms and costs of loans. This includes disclosing the annual percentage rate (APR), total finance charges, and repayment terms. TILA aims to promote transparency and help consumers compare loan offers.

Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act regulates the collection, dissemination, and use of consumer credit information. It ensures that consumers have access to accurate information in their credit reports and provides mechanisms for disputing inaccuracies. Lenders must adhere to FCRA guidelines when evaluating loan applications.

Equal Credit Opportunity Act (ECOA)

The Equal Credit Opportunity Act prohibits discrimination in lending based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Lenders must ensure that their lending practices comply with ECOA regulations and provide equal access to credit for all consumers.

Dodd-Frank Wall Street Reform and Consumer Protection Act

The Dodd-Frank Act established the Consumer Financial Protection Bureau (CFPB) to oversee and enforce consumer protection laws in the financial sector. The CFPB regulates various aspects of the installment loan market, including advertising practices, disclosure requirements, and fair lending practices.

State Regulations

In addition to federal regulations, installment loans are subject to state-specific laws and regulations. These can vary widely and may include interest rate caps, licensing requirements for lenders, and specific consumer protection measures. Borrowers should be aware of the regulations in their state and how they impact loan terms and availability.

The Future of Installment Loans

The installment loan market is poised for continued evolution, driven by technological advancements, regulatory changes, and shifting consumer preferences. Several trends are likely to shape the future of Lack of recent installment loan information:

Increased Use of Technology

Technology will continue to play a significant role in the installment loan market. Advances in AI, machine learning, and blockchain technology will enhance the lending process, making it more efficient, transparent, and secure. Digital platforms will become more prevalent, offering seamless and convenient loan management experiences.

Personalized Loan Products

As lenders gain access to more data and sophisticated analytics tools, they will be able to offer more personalized loan products. Lack of recent installment loan information, Tailored loan options that meet specific consumer needs and preferences will become more common, enhancing the overall borrowing experience.

Expansion of Alternative Credit Models

Alternative credit scoring models will gain traction, helping to expand access to credit for consumers with limited or no traditional credit history. These models will leverage diverse data sources to provide a more comprehensive assessment of creditworthiness.

Regulatory Adaptations

Regulatory frameworks will continue to evolve to address emerging challenges and opportunities in the installment loan market. Policymakers will focus on balancing consumer protection with innovation, ensuring that regulations keep pace with technological advancements and market trends.

Sustainable Lending Practices

Sustainability will become an important consideration in the installment loan market. Lenders will increasingly adopt environmentally and socially responsible practices, offering loan products that support sustainable initiatives and promote financial inclusion.

Increased Consumer Education

Financial literacy will remain a priority, with more efforts dedicated to educating consumers about installment loans and responsible borrowing practices. Enhanced financial education programs will empower consumers to make informed decisions and manage their finances effectively.

Conclusion

The lack of recent installment loan information poses a challenge for consumers seeking reliable data to make informed financial decisions. By understanding the types of installment loans available, their benefits, and the current state of information, borrowers can navigate this landscape more effectively. Financial institutions, regulators, and consumers must work together to bridge this information gap, ensuring that up-to-date and accurate data is accessible to all.