What is Credit Score Ranges: Top 10 FAQ's

Sign Up For Credit Repair

In today's financial landscape, credit score ranges is more than just a number; it is a pivotal element that can influence various aspects of our financial health. From securing a mortgage to getting approved for a credit card, understanding the nuances of credit score ranges is essential.

Understanding Credit Score Ranges: A Comprehensive Guide

This comprehensive guide delves deep into the intricacies of credit score ranges, providing valuable insights to help you navigate your financial journey effectively.

What is a Credit Score?

A credit score is a numerical representation of an individual’s creditworthiness, based on their credit history. These scores are typically generated by major credit bureaus such as Experian, Equifax, and TransUnion. The most commonly used credit scoring model is the FICO score, which ranges from 300 to 850.

Why is Your Credit Score Important?

A high credit score can open doors to financial opportunities, while a low score can limit your options. Lenders use your credit score to assess the risk of lending you money. A good credit score can result in lower interest rates, better loan terms, and even enhanced job prospects.

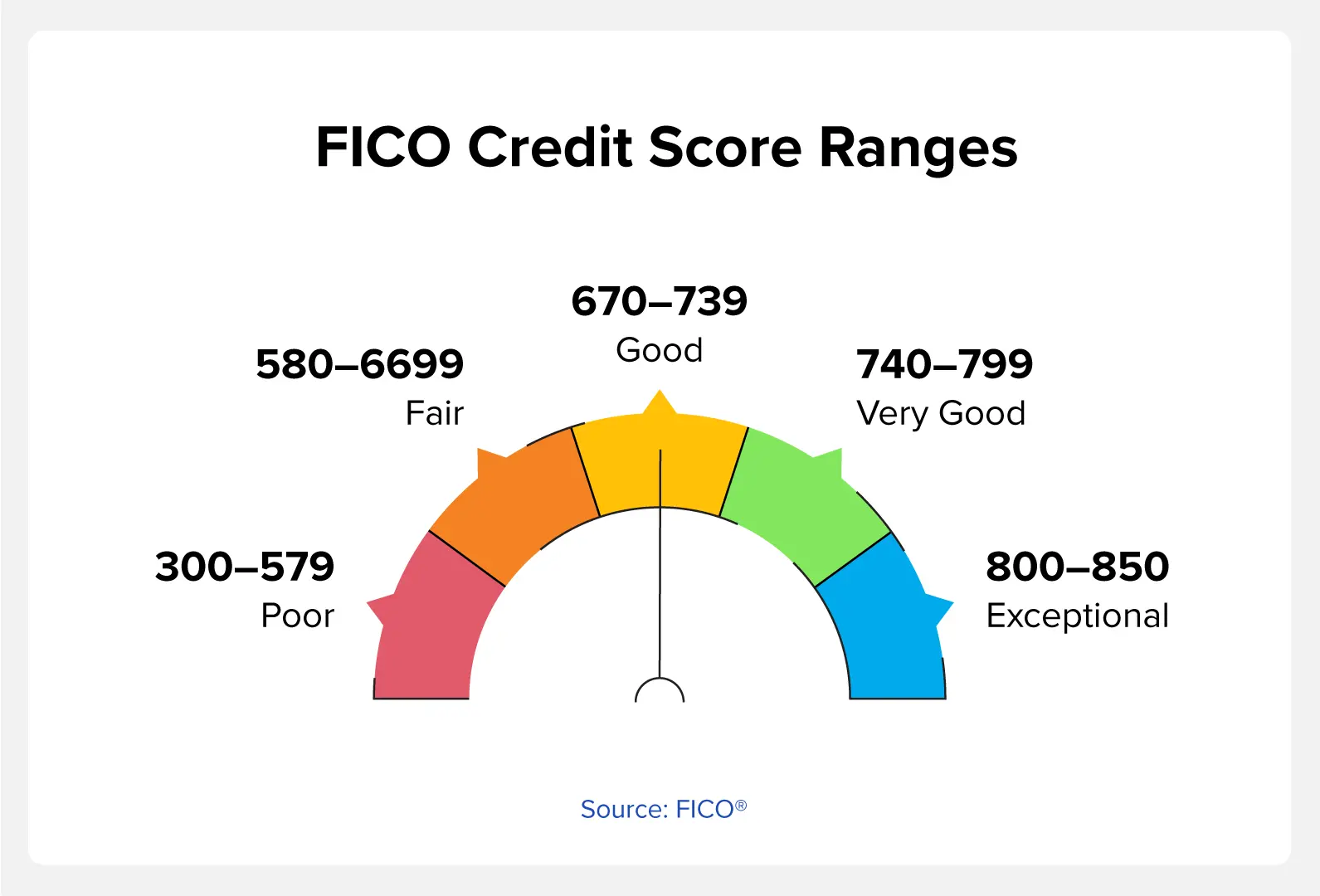

What Breaks Down Credit Score Ranges

Understanding the different credit score ranges can help you determine where you stand and what steps you need to take to improve your score. Here is a detailed breakdown of the typical credit score ranges:

What is Credit Score Range For Poor Credit: 300-579

Scores in this range are considered poor. Individuals with poor credit scores may struggle to get approved for loans or credit cards. If they do receive approval, it will likely be with high-interest rates and unfavorable terms. Factors that contribute to a poor credit score include missed payments, defaults, and a high debt-to-income ratio.

What is Credit Score Range For Fair Credit Score: 580-669

A fair credit score indicates that the individual is a moderate credit risk. While they may still face higher interest rates, they have more options available compared to those with poor scores. Consistently making on-time payments and reducing outstanding debt can help improve a fair credit score over time.

What is Credit Score Range For Good Credit Score: 670-739

A good credit score suggests a reliable borrowing history and financial responsibility. Individuals in this range have a strong chance of being approved for loans and credit cards with favorable terms. To maintain a good credit score, it’s important to keep credit card balances low and continue making timely payments.

Very Good Credit Score: 740-799

Those with very good credit scores are considered low-risk borrowers. They have access to the best interest rates and loan terms. Maintaining a very good credit score involves regular monitoring of credit reports and managing credit responsibly.

Exceptional Credit Score: 800-850

An exceptional credit score reflects an exemplary credit history. Individuals in this range have virtually guaranteed approval for any credit products they apply for, often with the best possible terms. They exhibit outstanding financial habits, including low credit utilization and a long history of on-time payments.

Factors Influencing Your credit score ranges

Understanding the factors that influence your credit score is crucial in managing and improving it. The key factors include:

Payment History for credit score ranges

Your payment history is the most significant factor, accounting for 35% of your credit score. Late or missed payments can have a substantial negative impact. Consistently making payments on time is vital for a healthy credit score.

Credit Utilization for credit score ranges

Credit utilization refers to the percentage of your total available credit that you are currently using. It makes up 30% of your credit score. Keeping your credit utilization below 30% is generally recommended to maintain a good score.

Length of Credit History for credit score ranges

The length of your credit history contributes 15% to your credit score. A longer credit history typically indicates stability and reliability, positively affecting your score.

New Credit for credit score ranges

New credit accounts for 10% of your score. Opening several new credit accounts in a short period can be seen as risky behavior and may lower your score.

Credit Mix for credit score ranges

Having a diverse mix of credit accounts, including credit cards, mortgages, and car loans, can positively influence your score. Credit mix accounts for 10% of your credit score.

How to Improve Your Credit Score

Improving your credit score requires time, patience, and a strategic approach. Here are some effective tips:

Pay Your Bills on Time for credit score ranges

Timely payment of bills is crucial. Set up reminders or automatic payments to ensure you never miss a due date.

Reduce Outstanding Debt at credit score ranges

Focus on paying down existing debt, especially high-interest debt. Consider consolidating debts to manage them more effectively.

Monitor Your Credit Report

Regularly check your credit report for errors or inaccuracies. Dispute any discrepancies you find to ensure your score reflects accurate information.

Limit New Credit Applications

Avoid applying for multiple new credit accounts in a short period. Each application can result in a hard inquiry, temporarily lowering your score.

Maintain Low Credit Utilization at credit score ranges

Aim to keep your credit utilization below 30%. Paying down balances and increasing your credit limit can help achieve this.

The Impact of Credit Scores on Your Financial Life

Your credit score impacts various aspects of your financial life beyond just loan approvals and interest rates. Here are some areas where your credit score can play a significant role:

Housing at credit score ranges

Landlords often check credit scores during the rental application process. A higher score can make it easier to secure a rental property.

Employment at credit score ranges

Some employers review credit scores as part of their hiring process. A strong credit score can enhance your job prospects, especially in roles involving financial responsibility.

Insurance Rates for credit score ranges

Insurance companies may use credit scores to determine premiums. A higher score can result in lower insurance costs.

Utility Services by credit score ranges

Utility providers sometimes require a credit check. A good credit score can help you avoid deposits and secure favorable terms.

Common Credit Score Myths

There are several misconceptions about credit scores. Understanding the truth behind these myths can help you make better financial decisions:

Myth 1: Checking Your Own Credit Score Lowers It

Checking your own credit score is considered a soft inquiry and does not affect your score. It is a good practice to monitor your score regularly.

Myth 2: Closing Old Accounts Improves Your Score

Closing old accounts can shorten your credit history and increase your credit utilization ratio, potentially lowering your score. It is often better to keep old accounts open.

Myth 3: Paying Off Debt Erases It from Your Credit Report

Paying off debt is beneficial, but it does not remove the history of the debt from your credit report. The account will show as paid, but the history will remain.

Myth 4: You Need to Carry a Balance to Build Credit

Carrying a balance is not necessary to build credit. Paying off your balance in full each month can help you avoid interest charges and build a strong credit history.

Tips for Long-Term Credit Health

Maintaining a good credit score is an ongoing process that requires diligence and good financial habits. Here are some additional tips for ensuring long-term credit health:

Diversify Your Credit

Having a mix of credit types, such as installment loans (e.g., mortgages, auto loans) and revolving credit (e.g., credit cards), can positively impact your credit score. Lenders like to see that you can manage different types of credit responsibly.

Keep Old Accounts Open

As mentioned earlier, the length of your credit history plays a significant role in your credit score. Keeping old accounts open, even if you don’t use them frequently, can help maintain a longer credit history.

Avoid Maxing Out Credit Cards

Maxing out your credit cards can significantly hurt your credit utilization ratio and your credit score. Try to keep your balances low relative to your credit limits.

Stay Informed About Your Credit Score

Use free credit monitoring services to keep tabs on your credit score and receive alerts about any significant changes. This can help you catch potential issues early.

The Role of Credit Counseling

If you’re struggling with debt or managing your credit, consider seeking help from a reputable credit counseling agency. These organizations can provide guidance on budgeting, debt management, and improving your credit score.

What is Credit Counseling?

Credit counseling involves working with a certified credit counselor to develop a plan for managing your finances and debt. These counselors can help you create a budget, negotiate with creditors, and establish a debt repayment plan.

Benefits of Credit Counseling

Credit counseling can provide numerous benefits, including personalized financial advice, reduced interest rates on debts, and a structured plan for becoming debt-free. Additionally, credit counseling can help you understand and improve your credit score.

Securing Your Financial Future

A solid credit score is essential for securing your financial future. By understanding credit score ranges, the factors that influence your score, and the steps you can take to improve it, you can make informed financial decisions and achieve greater financial stability.

Setting Financial Goals

Set clear financial goals, such as buying a home, saving for retirement, or paying off debt. A good credit score can help you achieve these goals by providing access to better financial products and terms.

Building an Emergency Fund

An emergency fund is a crucial part of financial planning. Having a cushion of savings can prevent you from falling into debt when unexpected expenses arise. Aim to save at least three to six months’ worth of living expenses.

Investing in Your Future

Consider investing in assets that can grow over time, such as stocks, bonds, or real estate. Building wealth through investments can provide financial security and enhance your overall financial health.

Education and Financial Literacy

Educate yourself about personal finance and credit management. The more you know, the better equipped you’ll be to make sound financial decisions. There are numerous resources available, including books, online courses, and financial advisors.

Conclusion

Understanding and managing your credit score is essential for achieving financial stability and accessing the best financial products. By knowing the different credit score ranges and the factors that influence them, you can take proactive steps to improve your score and secure your financial future.

- Poor: 300–579 for FICO, 500–600 for VantageScore

- Fair: 580–669 for FICO, 601–660 for VantageScore

- Good: 670–739 for FICO, 661–780 for VantageScore

- Very good: 740–799 for FICO

- Excellent: 800+ for FICO, 781–850 for VantageScore