The Ultimate Guide to 609 Dispute Letter: 35 Key Insights

Introduction:

When it comes to cleaning up your credit report, the 609 dispute letter is one of the most powerful tools at your disposal. Named after Section 609 of the Fair Credit Reporting Act (FCRA), this letter is your formal request to the credit bureaus to verify the accuracy of items listed on your credit report.

Understanding the 609 Dispute Letter

What is a 609 Dispute Letter?

A 609 dispute letter is a formal request you send to the credit bureaus to validate information on your credit report. If they cannot verify the information, they are required by law to remove it. This makes the 609 dispute letter an essential tool in credit restoration services.

How Does the 609 Dispute Letter Work?

The 609 dispute letter works by leveraging your right to request validation of the information on your credit report. When you send this letter to the credit bureaus, they must investigate the disputed items and provide evidence of their accuracy. If they cannot, they must remove the items.

Why Use a 609 Dispute Letter?

Using a 609 dispute letter can help you remove inaccurate, unverifiable, or incomplete information from your credit report, thereby improving your credit score. This is a crucial step in credit fixing services and credit restoration.

How to Write a 609 Dispute Letter

Step 1: Obtain Your Credit Reports

Before you can dispute any items, you need to know what’s on your credit report. Obtain copies of your reports from the three major credit bureaus: Experian, Equifax, and TransUnion.

Step 2: Identify the Items to Dispute

Carefully review your credit reports for any inaccurate, incomplete, or unverifiable information. Highlight these items as they will be the focus of your 609 dispute letter.

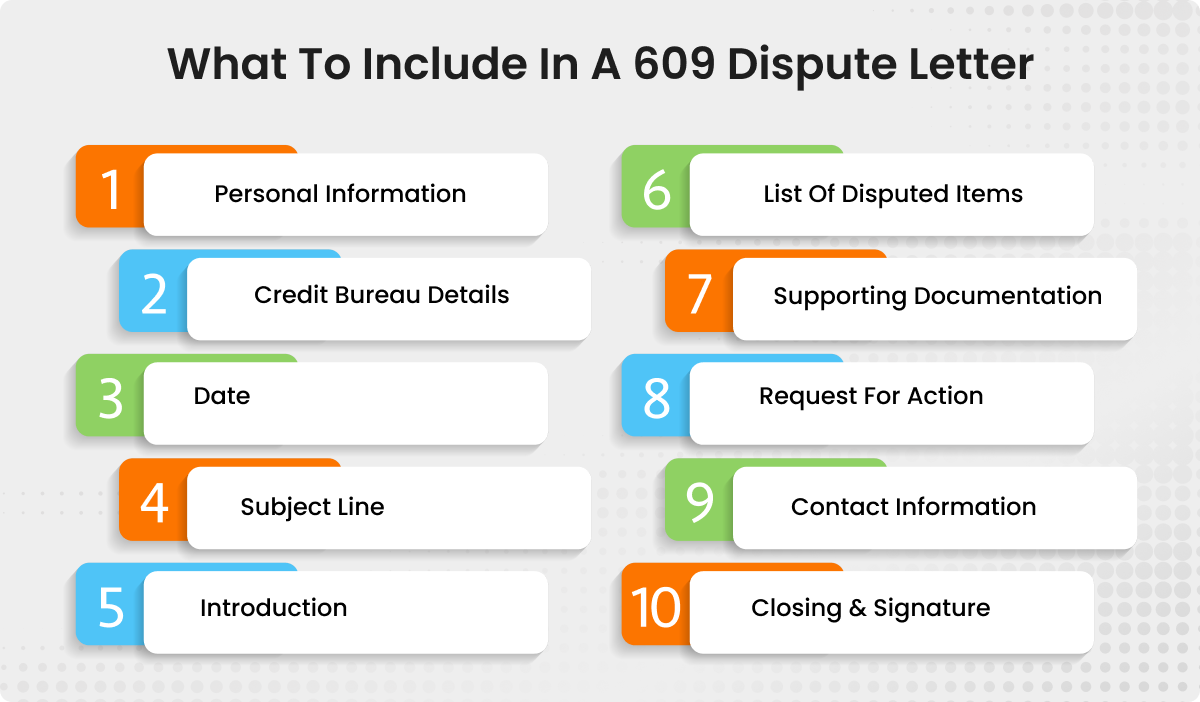

Step 3: Draft Your 609 Dispute Letter

When drafting your 609 dispute letter, be clear and concise. Include your personal information, the items you are disputing, and why you believe they are inaccurate. Here is a sample template to get you started:

[Your Name]

[Your Address]

[City, State, Zip Code]

[Email Address]

[Date]

[Credit Bureau Name]

[Credit Bureau Address]

[City, State, Zip Code]

Dear [Credit Bureau Name],

I am writing to dispute the following information on my credit report. According to Section 609 of the Fair Credit Reporting Act, I am requesting that you verify these items. If you cannot verify them, they must be removed.

[List each item you are disputing, including account names, numbers, and the reason for dispute]

I have included copies of my credit report with the disputed items highlighted. Please investigate and correct these discrepancies.

Sincerely,

[Your Name]

Step 4: Gather Supporting Documentation

Include any supporting documentation that can help validate your dispute, such as payment records, correspondence with creditors, or any other relevant information.

Step 5: Send Your Letter

Send your 609 dispute letter and supporting documentation to the credit bureaus via certified mail with a return receipt requested. This ensures you have proof that the credit bureaus received your dispute.

What to Expect After Sending a 609 Dispute Letter

Credit Bureau Response Time

Credit bureaus are required to investigate your dispute within 30 days of receiving your letter. They will contact the creditor for verification and then respond to you with their findings.

Possible Outcomes

- Item Verified: The credit bureau confirms the accuracy of the item, and it remains on your report.

- Item Deleted: The credit bureau cannot verify the item, and it is removed from your report.

- Item Updated: The information is updated to reflect accurate details.

Following Up

If you do not receive a response within 30 days, follow up with the credit bureau. Persistence is key in the credit repair process.

Additional Tips for Success with 609 Dispute Letters

Be Organized

Keep a detailed record of all your correspondence with the credit bureaus, including copies of your letters, proof of mailing, and any responses you receive.

Be Persistent

If your initial dispute is unsuccessful, don’t give up. Sometimes it takes multiple attempts to achieve the desired outcome. Each time you dispute, ensure you are providing as much evidence as possible to support your claim.

Use Professional Help

Consider using a credit restoration company if you find the process overwhelming. These companies have experience with credit disputes and can handle the process on your behalf.

Common Questions About 609 Dispute Letters

What is the Difference Between a 609 Dispute Letter and a 611 Dispute Letter?

A 609 dispute letter is a request for the credit bureau to validate information, while a 611 dispute letter is used to dispute the results of an investigation if you believe the information is still inaccurate.

Can a 609 Dispute Letter Remove Accurate Information?

No, a 609 dispute letter cannot remove accurate information from your credit report. It is designed to challenge items that are inaccurate, incomplete, or unverifiable.

How Often Can I Send a 609 Dispute Letter?

There is no limit to how often you can send a 609 dispute letter, but it is advisable to wait for the outcome of each dispute before sending another.

Do 609 Dispute Letters Work?

Yes, 609 dispute letters can be effective if the disputed items are truly inaccurate or unverifiable. The key is to provide sufficient evidence to support your claims.

Enhancing Your Credit Restoration Efforts

Use Credit Restoration Services

Utilizing credit restoration services can significantly enhance your credit repair efforts. These services have the expertise to handle disputes and negotiate with creditors on your behalf.

Employ Credit Fixing Services

Credit fixing services can provide personalized strategies to address your unique credit issues, helping you to improve your credit score more effectively.

Explore Credit Report Repair Companies

Engage with reputable credit report repair companies to take advantage of their professional knowledge and experience in dealing with credit disputes.

Key Takeaways for Using 609 Dispute Letters

The Importance of Accuracy

Ensure all information in your 609 dispute letter is accurate and supported by evidence. This increases the likelihood of a successful dispute.

The Power of Persistence

Persistence is crucial in the credit repair process. If your initial dispute is not successful, continue to follow up and provide additional evidence as needed.

Professional Assistance

Don’t hesitate to seek professional assistance if needed. Credit restoration services and credit report repair companies can provide valuable support in your credit repair journey.

Additional Strategies for Credit Repair

Pay for Removal Letters

A pay for removal letter is a request to a creditor to remove a negative item from your credit report in exchange for payment. This can be an effective strategy if you have outstanding debts.

Good Credit Repair Services

Engaging a good credit repair service can provide you with expert guidance and support throughout the credit repair process.

Credit Cleaning Services

Utilize a credit cleaning service to help remove negative items from your credit report and improve your credit score.

Credit Score Repair

Focus on strategies for credit score repair, such as reducing debt, making timely payments, and maintaining a low credit utilization rate.

Frequently Asked Questions About Credit Repair

How Long Does an Eviction Stay on Your Record?

An eviction can stay on your credit report for up to seven years. However, disputing inaccuracies and providing evidence of payment can help remove it sooner.

What Credit Rating Do You Start With?

Most people start with a credit rating of around 300 to 500. Building a positive credit history can improve this score over time.

Does Breaking a Lease Hurt Your Credit?

Yes, breaking a lease can hurt your credit if the landlord reports the unpaid rent to the credit bureaus or takes legal action against you.

How to Repair Your Credit on Your Own

To repair your credit on your own, focus on disputing inaccuracies, making timely payments, reducing debt, and maintaining a low credit utilization rate.

Conclusion: The Power of the 609 Dispute Letter

A 609 dispute letter is a powerful tool for improving your credit report and, ultimately, your financial health. By understanding the process, following the steps outlined in this guide, and utilizing additional strategies like credit restoration services and credit fixing services, you can effectively remove inaccurate information from your credit report and achieve a healthier credit score.

Remember, persistence and organization are key to success in the credit repair process. Keep detailed records of your disputes, follow up regularly, and don’t hesitate to seek professional help if needed. With the right approach, you can leverage the power of the 609 dispute letter to enhance your credit profile and enjoy the benefits of a strong credit score.

For expert assistance, consider contacting CRO Accounting and Credit Repair Services at CroMiami.com, calling (877) 590-9832, or emailing Info@cromiami.com. Their professional services can help guide you through the complexities of credit restoration and ensure you achieve the best possible outcomes for your credit health.

How to Leverage a 609 Dispute Letter for Different Credit Issues

Dealing with Timeshare Foreclosure

How to remove timeshare foreclosure from your credit report can be challenging, but a 609 dispute letter can be effective if the foreclosure is inaccurately reported. Start by gathering all documentation related to the timeshare, including the original purchase agreement, payment history, and any correspondence with the timeshare company.

In your 609 dispute letter, clearly state that you are disputing the foreclosure entry due to inaccuracies. Include copies of your supporting documents to strengthen your case. If the credit bureaus cannot verify the foreclosure, they must remove it from your credit report.

Removing Repossession Entries

If you are wondering how to get a repo off your credit, a 609 dispute letter can be an invaluable tool. First, obtain all records related to the repossession, including payment history and communication with the lender. If you find any discrepancies, include these in your 609 dispute letter and request the credit bureau to validate the information. If they cannot, the repossession entry must be removed.

Addressing Loan Shark Loans

Loan shark loans often come with predatory terms that can severely damage your credit. To mitigate this, use a 609 dispute letter to challenge any inaccuracies in the reporting of these loans. Provide evidence of predatory lending practices if available, and clearly outline these in your letter. If the credit bureau cannot verify the loan details, they are obligated to remove the negative entry.

Correcting Eviction Records

An eviction can significantly impact your credit score. If you find inaccuracies in the eviction entry on your credit report, a 609 dispute letter can help. Gather all related documents, such as court records and payment receipts, and include these in your dispute letter. State explicitly that you are challenging the accuracy of the eviction record. If the credit bureau cannot verify the eviction, it must be removed from your report.

Maximizing the Effectiveness of Your 609 Dispute Letter

Using Certified Mail

Sending your 609 dispute letter via certified mail ensures you have proof of delivery. This can be crucial if you need to follow up with the credit bureaus or escalate your dispute.

Including a Copy of Your Credit Report

Always include a copy of your credit report with the disputed items highlighted. This helps the credit bureau quickly identify the entries you are challenging.

Keeping Detailed Records

Maintain a file with copies of all your correspondence, including your 609 dispute letter, proof of mailing, and any responses from the credit bureaus. This documentation can be useful if you need to escalate your dispute.

Following Up Regularly

If you do not receive a response within 30 days, follow up with the credit bureau. Persistent follow-up can significantly increase your chances of a successful dispute.

The Role of Professional Credit Repair Services

Engaging Credit Restoration Services

Credit restoration services can handle the entire dispute process on your behalf, ensuring all legal requirements are met and increasing the likelihood of a successful outcome. These services are particularly useful if you have multiple items to dispute or if the process feels overwhelming.

Choosing the Right Credit Repair Company

Select a reputable credit restoration company that has a proven track record of success. Look for companies with positive reviews and transparent pricing. Avoid companies that make unrealistic promises, such as guaranteeing the removal of accurate information from your credit report.

Utilizing Credit Report Repair Companies

Credit report repair companies specialize in disputing inaccurate entries on your credit report. They have the expertise to identify errors and the legal knowledge to challenge these effectively. Using such companies can save you time and improve your chances of a successful dispute.

Common Mistakes to Avoid When Using a 609 Dispute Letter

Not Including Sufficient Evidence

One of the most common mistakes is failing to include enough evidence to support your dispute. Always provide as much documentation as possible to back up your claims.

Being Too Vague

Your 609 dispute letter should be specific and detailed. Clearly identify the items you are disputing and explain why you believe they are inaccurate.

Failing to Follow Up

Do not assume that the credit bureau will handle your dispute without follow-up. Keep track of deadlines and follow up if you do not receive a timely response.

Ignoring Professional Help

If you are struggling with the dispute process, do not hesitate to seek professional assistance. Credit restoration services and credit report repair companies can provide valuable support and expertise.

Enhancing Your Credit Beyond Disputes

Regular Monitoring of Your Credit Report

Regularly monitoring your credit report can help you catch errors early and dispute them promptly. Many services offer free credit monitoring, which can alert you to changes in your credit report.

Using a Credit Rating Calculator

A credit rating calculator can help you understand how different actions, such as paying down debt or disputing inaccuracies, will impact your credit score. This can be a valuable tool in planning your credit repair strategy.

Seeking Credit Help

If you need guidance on improving your credit, seek out credit help services. These services can provide personalized advice and strategies to help you achieve your credit goals.

Understanding CPNs

A CPN (Credit Privacy Number) is often marketed as a way to start fresh with a new credit identity. However, using a CPN can be illegal and is not recommended. Instead, focus on legitimate credit repair strategies.

Leveraging Other Dispute Letters

Pay for Delete Letter

A pay for delete letter is a request to a creditor to remove a negative item from your credit report in exchange for payment. This can be an effective strategy if you have outstanding debts that you are willing to pay in exchange for a clean credit report.

611 Dispute Letter

If your initial 609 dispute letter is unsuccessful, you can use a 611 dispute letter to challenge the results of the credit bureau’s investigation. This letter should clearly outline why you believe the item is still inaccurate and request a re-investigation.

Using a 609 Dispute Letter for Identity Theft

If you are a victim of identity theft, a 609 dispute letter can help remove fraudulent accounts from your credit report. Include a copy of your identity theft report and any other relevant documentation with your dispute letter.

Conclusion: Mastering the 609 Dispute Letter

Mastering the use of a 609 dispute letter can significantly improve your credit report and overall financial health. By understanding the process, being persistent, and utilizing professional credit restoration services when necessary, you can effectively remove inaccurate information from your credit report.

Final Thoughts: The Power of the 609 Dispute Letter

The 609 dispute letter is a powerful tool in your credit repair arsenal. It empowers you to challenge and remove inaccurate information from your credit report, paving the way for a healthier credit score. Remember, the key to success lies in being thorough, organized, and persistent. Keep detailed records, follow up regularly, and don’t hesitate to seek professional assistance if needed.

For expert help, contact CRO Accounting and Credit Repair Services at CroMiami.com, call (877) 590-9832, or email Info@cromiami.com. Their professional services can guide you through the complexities of credit repair and help you achieve the best possible outcomes for your credit health.

With the right approach and the power of the 609 dispute letter, you can take control of your credit report and enjoy the benefits of a strong credit score.